There is a shortage of quality premises in the capital's business centers

Moscow's business clusters are in a frenzy: within the Moscow Ring Road, average rental rates are at record levels, and the office vacancy rate, despite record new space being added, has approached a historic low. Empty spaces in new business centers are quickly being cleared from the market, keeping vacancy rates critically low.

"In Moscow, the average rental rate for high-quality offices within the Moscow Ring Road has increased by 38% year-on-year, reaching 35,000 rubles per square meter excluding VAT and operating expenses, a historic high," said Irina Khoroshilova, head of the office real estate department at consulting firm CORE.XP. In the capital's central business district and the Moscow-City cluster, rental rates have increased by 44% year-on-year, reaching an average of 56,000 rubles per square meter in the third quarter of this year.

"The current rental rate level is a direct consequence of the shortage of quality space," the expert emphasized. According to her, it was primarily expensive space in new projects that entered the market, while more affordable smaller lots virtually disappeared from the supply. The significant increase in mid-size space—ranging from 1,000 to 3,000 square meters—also contributed to the growth of the weighted average.

According to Khoroshilova, Prime-class office rents have increased by 58% year-on-year, to 72,000 rubles per square meter per year, while Class A rents have increased by 35%, to 47,000 rubles. Class B+ office rents have increased by 9%, to 31,000 rubles, and Class B- office rents have increased by 92%, to 28,500 rubles.

"Rental growth, typically faster than expected, is typical for high-quality properties. Tenants choose established business districts and are prepared to wait for suitable space for expansion—this creates a waiting list for high-quality properties in high-demand locations. Business centers in key business locations with developed infrastructure and high service levels gain a competitive advantage, while offices in less attractive locations often experience near-zero rental growth," noted Valentin Kusov, Deputy Director of the Office Real Estate Department at Nikoliers.

"The most affordable rates are traditionally found in locations outside the Moscow Ring Road," said Stepan Zaytsev, Deputy Commercial Director of Business Club. He believes that historical highs were reached in 2024, and by October 2025, the market had already entered a phase of stagnation and correction. The main factors driving these highs are a structural shortage of quality space in the completed market segment. Low vacancy rates in existing Class A and B+ buildings over a long period allowed landlords to dictate terms. Furthermore, high demand from companies seeking high-quality offices, especially in prime locations (within the Third Transport Ring), played a role. Office owners were forced to raise rents due to rising operating costs and inflationary pressure.

"The volume of rental transactions has fallen by a third over the past nine months, driven by a shortage of quality inventory and record-high asking rates. Sales remain the main market driver today," emphasized Vladislav Stepanov, CEO of ESVE Group. He believes the profile of interested parties is changing, and the demand structure is becoming more balanced. There's no longer a significant bias toward the public sector, as some needs have been met. Companies from the energy and fuel sectors are active, and demand from IT players remains strong.

This year, the main drivers of demand for office space, according to Maria Zimina, Director of the Office Real Estate Department at NF Group, were companies in the technology, media, and telecommunications sectors (21%), as well as organizations operating in the banking, financial, and investment sectors (21%). Manufacturing companies ranked third in terms of demand (16%).

"From January to October, total demand (rental and purchase) amounted to 1,077,000 square meters," Zaitsev noted. He added that supply is actively growing due to new construction. Sales began in 2025 in 29 new projects (867,000 square meters of Class A and B+ space), double the previous year's figure. The average listing price for office blocks as of October 1 was 458,000 rubles per square meter (excluding VAT), 7% higher than the previous year. The price range is wide—from 167,000 to 1.3 million rubles per square meter.

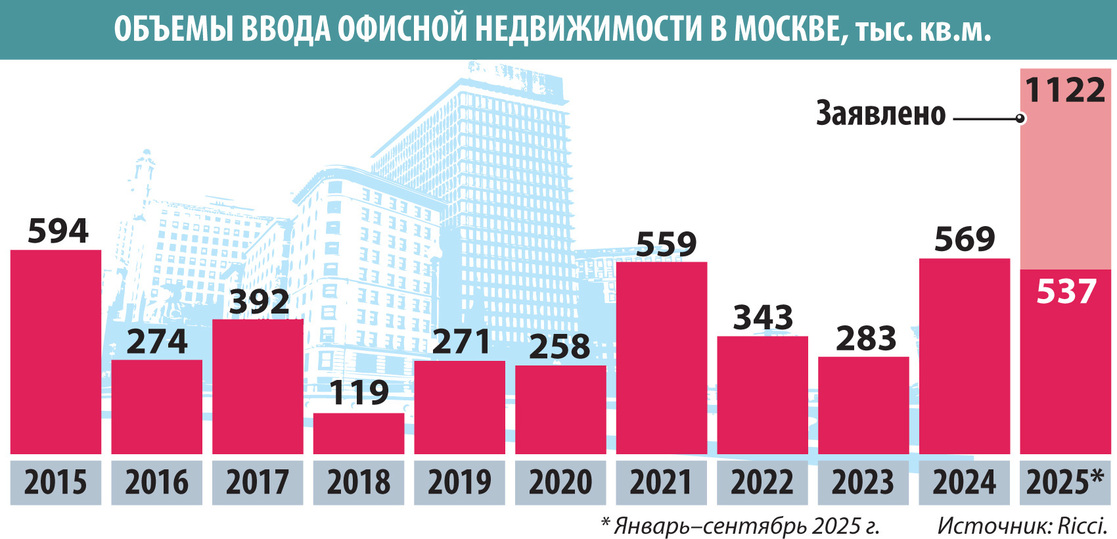

According to Ricci, Moscow developers announced the completion of approximately 585,000 square meters of office space in the fourth quarter. This, combined with the 537,000 square meters already delivered in January–September, will bring the total office space supply to 1.12 million square meters (see chart). This would be the highest figure since 2014, when 1.29 million square meters were built. However, construction deadlines for individual projects are often postponed until the following year in November–December, so the final figure may be lower.

However, even with such substantial volumes, the vacancy rate is not growing: high demand for office purchases and leases is further declining. By October, it had fallen to 5.5% and continues to approach the historic low of 2007, Zimina reported. In Class A, the rate has decreased by 0.1 percentage points since the beginning of the year, to 7.1%, and in Class B, by 0.5 percentage points, to 4.7%.

"In the current market environment, most properties are being commissioned fully or partially occupied, and the volume of available space from new construction is insufficient to meet existing demand," Zimina noted. She doesn't expect a significant increase in the share of available space: with a shortage of office space for rent, a limited supply of space under construction, and high demand, most office space is quickly absorbed by the market. In the coming years, she estimates that the share of new offices coming online for rent will amount to no more than 5-20% of the total volume of new office space, while the bulk will be for sale.

According to Kusov's forecast, base rental rates will continue to rise through 2030, both through vacant inventory, at an average annual rate of 7%, and through implicit renegotiations of contract renewals to replace insolvent tenants, at an average rate of 15-20%. He expects the vacancy rate for 2025-2030 to be 5.3%.

Published in the Moskovsky Komsomolets newspaper, No. 29645, November 11, 2025

Newspaper headline: Moscow can't seem to satisfy its hunger for office workers.

mk.ru