America's Lever Flips: What We Learned After the September Fed

The United States Central Bank is under pressure from the president. Trump has set a course for looser monetary policy. That means higher inflation, just to prevent unemployment from rising. It's worth not suggesting the initial reaction of financial markets.

There is agreement on one thing: in the middle – and maybe also in longer term This was a landmark meeting of the Federal Open Market Committee . Let's start with the facts:

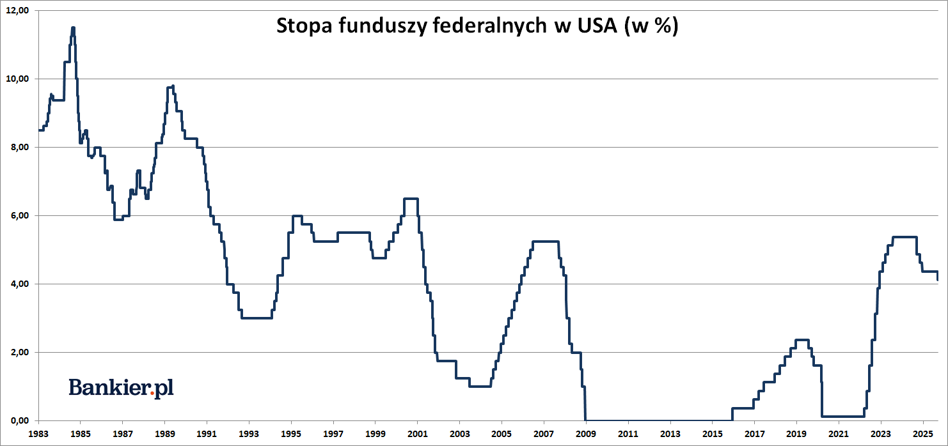

- The FOMC lowered the interest rate in line with market expectations. federal funds rate by 25 basis points. This was the first cut after a nine-month monetary "pause".

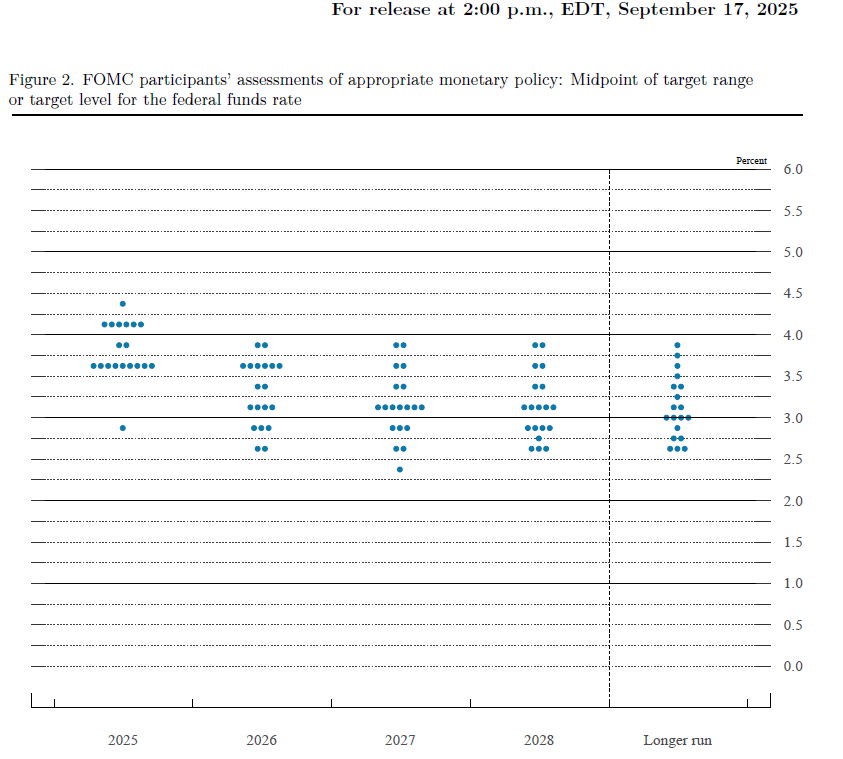

- The fedokropki contained a majority for the next two 25 basis point rate cuts in 2025. This means that cuts in interest rates are almost certain October and December.

- For a deeper – 50 basis point – rate cut voted the new presidential nominee Stephen Miran, who joined the Board of Governors on the day the election began September meeting

- Members The Committee slightly REDUCED their forecasts for the unemployment rate and They have RAISED next year's PCE inflation forecast.

- IN The FOMC statement included new wording drawing attention to slowdown in the labor market and rising inflation. But the most important thing is that The Committee concluded that the "downside risk of employment has increased" (risk)

For this there was a rather bland speech by Chairman Powell. He still insisted that monetary policy was "restrictive" (which in a situation of rising inflation and record low credit spreads is the least debatable thesis) and that will move towards a neutral policy. Powell, on the other hand, quite clearly rejected the demand to cut interest rates by 50 basis points immediately.

- In the short term, the risk of higher inflation has increased, while The risk of a deterioration in the labor market has increased, Powell added. the wording combined with the dot graph, in my opinion, announces the beginning of the entire cycle interest rate cuts at the Federal Reserve.

According to the "fedokropki" the funds rate will be higher by the end of 2027. federal will fall to around 3% and will also remain at this level "in long term", where the rate perceived as neutral by the FOMC is 3.0%. roughly in line with market expectations. With the only minor difference being that the market sees it dropping even below 3% in 2026. But these are details, and even The "fedokropki" themselves should not be approached with reverence, because they are rarely when they announce what the FOMC will actually do.

Second, the Federal Reserve begins an easing cycle monetary policy in conditions where FOMC members themselves anticipate a higher than They predicted inflation and a lower unemployment rate in June. This is patently absurd! In such a situation, a responsible central bank would either refrain from making decisions regarding rates, or even risk a price increase. But under no circumstances a price reduction, which after all, it stimulates inflation and is intended to stimulate the economic situation and This will strengthen the demand for labor (and consequently lower unemployment). Moreover, according to the median forecast of members FOMC core PCE inflation is expected to remain above the 2 percent target until 2028 The Committee has therefore made it clear that, within its "dual mandate" , it now prioritizes the goal of maximizing employment over the inflation target.

Gentlemen, let's count the votesThis leads us to equally obvious conclusion number three: the September FOMC decision was purely political. And it's not about monetary policy (because that would lead to keep FFR unchanged), but pressure coming from the White House. Donald Trump's seven-member Board of Governors He already has three of his own people. Including Stephen, who was appointed just on Wednesday Mirana, who voted against Chairman Powell on the 'good morning' and voted for a 50-point reduction in the FFR. Formally, Mr. Miran still holds position in the White House, so his declarations of "independence" from the president are pure farce. In addition, we have Michelle Bowman and Christopher Waller, who in In July, they voted to cut rates against the majority of the Committee.

Add to that President Trump's attempted removal Governor Lisa Cook , which have so far been blocked by Court of Appeal. But the case will probably go to the Supreme Court, where most of the judges was nominated by the Republican Party. Furthermore, her term ends in May 2026. Chairman Powell's term , replaced by Donald Trump he will probably choose someone more submissive and cutting rates faster at the president's request. Then, in a few months, up to 5 out of 7 members The Board of Governors may be "Trump's men." And they will have a dominant position (but not necessarily a majority) on the 12-member Open Market Committee, which rotates also includes the presidents of the four local Fed branches and the head of the branch New York.

It may therefore turn out that in 2026 the FOMC will cut rates percentage points faster and deeper than the current dot plot would suggest. President Trump will simply replace the "dots" with more "dove-like" ones. in the long run it will mean less independence for the Federal Reserve from the executive branch in Washington. This arrangement always ends the same way: higher inflation.

What will the market say?The first reactions of financial markets to FOMC announcements are often confusing. Initially, the markets reacted very optimistically: the dollar weakened against the euro, and stock market indices started to rise. Later, the market turned profit-taking mode and quickly erased the initial moves. Wednesday's session on Wall Street ended slightly below the line , and the EUR/USD exchange rate fell to around USD 1.18, retreating from this year's newly conquered peak (1.1920).

We will know the actual reaction of the markets today and in the following days. It is also worth bearing in mind that almost exactly investors have been discounting such a scenario for the past few weeks and may act according to the principle: buy the rumors, sell the facts. It is probably no coincidence that in recent days and For weeks we have been observing new records in gold prices .

In summary, the Fed's new monetary policy will be aimed at maintaining low unemployment and high satisfaction for President Trump. In the short term This could support stock markets by raising the nominal profits of listed companies. At the same time, tough times may lie ahead for bond investors. also a clear "green light" for precious metals and presumably as well as industrial raw materials. The biggest victim will be the US dollar.

bankier.pl